Tax Benefits of Employer-provided Health Screenings

A practical guide using the $2,999 Everlab Protocol Program as an example

Disclaimer

This document provides general information only and does not constitute tax, legal, or financial advice. The information is based on the Income Tax Assessment Act 1997, the Fringe Benefits Tax Assessment Act 1986, and publicly available ATO guidance as at the date of preparation.

Tax law is subject to change. The examples use simplified assumptions (25% company tax rate, 37% marginal tax rate, Type 1 gross-up factor of 2.0802) and may not reflect actual outcomes. Employers and employees should consult a qualified tax advisor to assess their specific situation.

Any FBT liability rests with the employer. No warranty is given as to the accuracy or completeness of this information, and no liability is accepted for any loss arising from reliance upon it.

What is it?

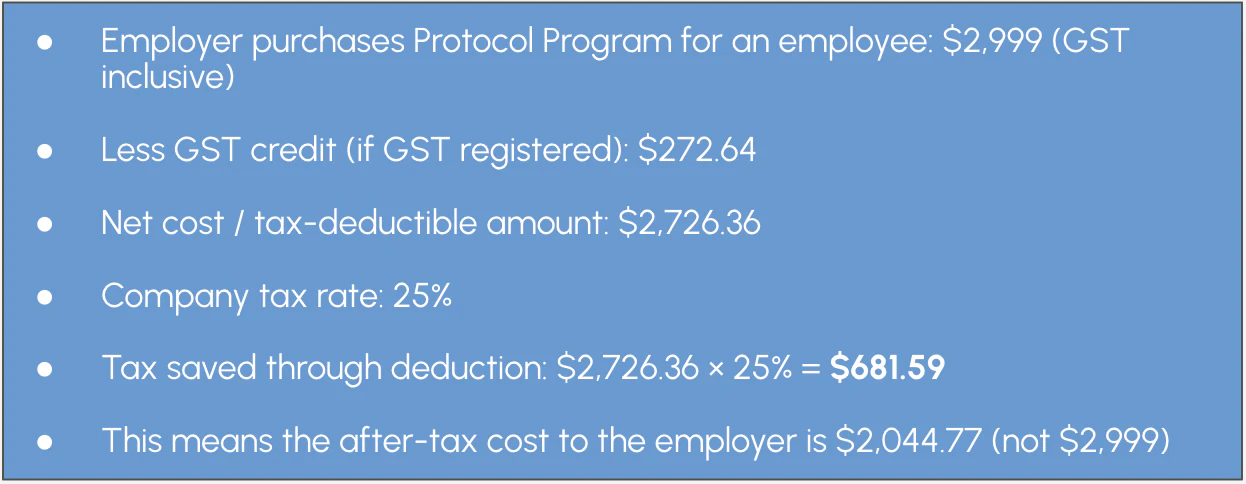

A tax deduction reduces the employer's taxable income. When a business spends money on legitimate business expenses, that amount is subtracted from revenue before calculating company tax.

How does it apply to health screenings?

Under section 8-1 of the Income Tax Assessment Act 1997, employers can generally deduct expenses incurred in running their business. Health screening costs for employees are typically deductible because they relate to maintaining a productive workforce.

Example

What is it?

Fringe Benefits Tax (FBT) is a tax the employer pays when they provide non-cash benefits to employees. It exists to ensure employees can't avoid income tax by receiving benefits instead of salary. The FBT rate is 47%, and it applies to a 'grossed-up' value (approximately double the benefit value).

Why is there an exemption for health screenings?

Under section 58M(1)(c)(ii) of the FBTAA 1986, 'work-related medical screenings' are exempt from FBT. This recognises that preventive health screening programs benefit workplaces and should not be discouraged by additional tax.

What qualifies for the exemption?

The screening must meet these criteria:

- It assesses whether employees have or are at risk of work-related health conditions

- It is conducted by a qualified medical professional

- It is available to all employees with similar roles/risks

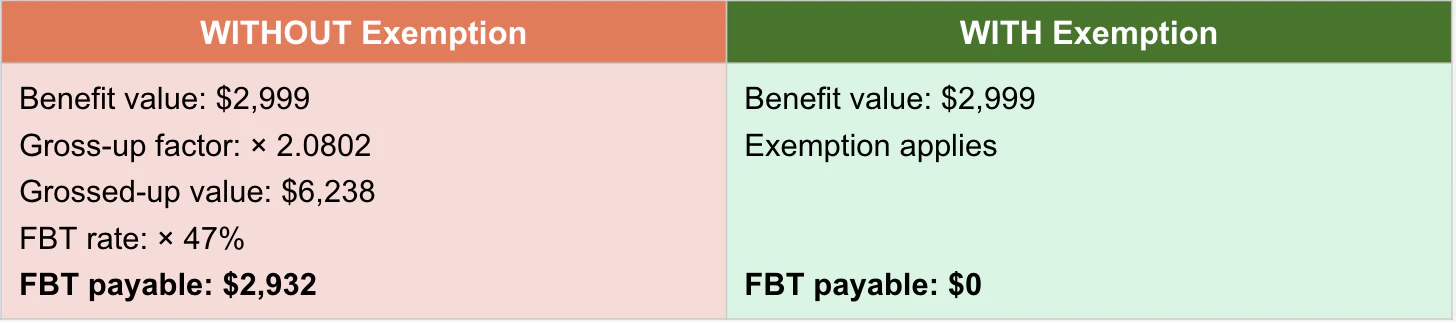

Example: With vs Without the Exemption

Key point: Without the exemption, the employer pays almost as much in FBT ($2,932) as the cost of the program itself ($2,999). The exemption eliminates this entirely.

Note: The gross-up factor of 2.0802 applies to GST-registered employers. A lower rate applies for non-GST registered entities.

What is it?

Salary sacrifice is an arrangement where an employee agrees to receive less cash salary in exchange for the employer providing a benefit. The benefit is paid from the employee's pre-tax income.

How does it benefit the employee?

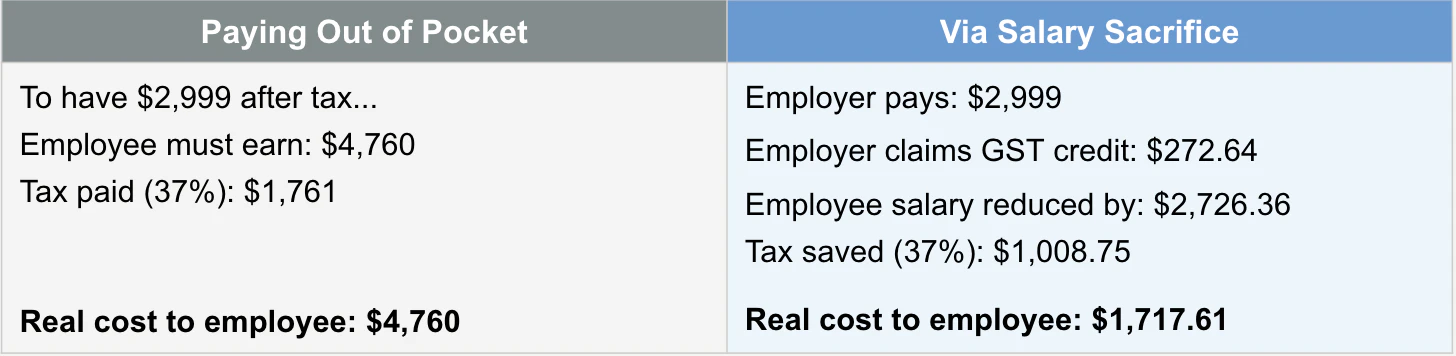

Normally, if an employee wanted to pay for a $2,999 health screening themselves, they would need to earn that money, pay income tax on it, and then spend what's left. With salary sacrifice, the amount is deducted before income tax is calculated.

Example: Employee on $120,000 salary (37% marginal tax rate)

Key point: Salary sacrifice saves the employee $1,008.75 in this example. However, this only works if the FBT exemption applies – otherwise the employer would need to pay FBT, which may negate the benefit.